AutoMobility Insights - November 2024 edition

The latest news from the automotive industry curated and commented by the experts at Corporate Value Associates (CVA).

In partnership with

Corporate Value Associates

Corporate Value Associates is a Global Strategy Boutique supporting market leaders in creating value through its customer-centric approach.

Even within our period of unprecedented massive change, the current weeks are probably outstanding. The Paris Motor Show reflected the still glamorous side of vehicles, but also the questioning about how European OEMs can make sure to still be around in 2035. While showcasing an impressive presence of Chinese OEMs, who position as a real alternative to products of incumbent OEMs, and not "low-cost complements". Also Tesla increases pressure on traditional OEMs, as it has managed to lower costs and increase margins, which now allows it to decrease New Car prices and double down on the "race to the bottom", actually making its Model 2 superfluous. A bold strategy, but still more realistic than its ambitions in Autonomous Driving, where additional proof points (starting to be delivered by Cruise Automation, Waymo, Baidu...) are required to actually believe. All of these BEV-driven changes rely considerably on the most important, but least understood, component of the EV, namely the battery, where it seems unlikely that a new magic technology will dispense us from working out how to deal with the current lithium-based one. All of these topics have found their way into the latest Webinar of the Qorus-CVA Mobility Community, where new and used vehicle price evolution and the impact on EV residual values have been discussed at length. Many other topics are emerging in the AutoMobility Ecosystem, including how OEMs will succeed to face the former long-term challenges, which have now become short-term urgencies. We will report on this in next month's edition.

Lessons from the Paris Motor Show

The Paris Motor Show (14-20th October) reflected the Transformation of the Industry. Shiny and impressive new models, a festive mood tried to overcome a certain gloom after a number of profit warnings by European OEMs. The Motor Show also had a record number of new Chinese exhibitors, showing their latest vehicle models, all ready to be sold in Europe. In this context, the exhibitors fought for the attention of over 500,000 visitors. The feedback from many European OEMs was rather mitigated, with some exceptions like Renault, which launched a series of new all-electric models. Indulging in tradition and nostalgia, with many ICE vehicles on display, the challenge of achieving tightening CO2 emission targets in 2025 was in practically all discussions.

Chinese OEMs, on the other hand, often showcased their products with a clear premium ambition, including massive flagship SUVs, but still at a very affordable price. Hence showing their intention to position on "premium value for money" rather than low cost. This also explains an apparent scarcity of affordable city cars with reasonable range. The closest here is perhaps the shared offer from Stellantis with Leapmotor and the new Renault models R4 and R5. The long-anticipated Skoda Elroq remains, with a base price of €33,900, far above the critical €25,000 mark. Alongside new vehicle releases, many discussions centered around the evolution of EV residual values and the best management of increasing uncertainty on regulation, volumes, and prices.

CVA perspective:

The Paris Motor Show provided a unique opportunity to witness a range of automotive trends all in one place. As visitors moved through the extensive exhibitor lineup, the question, "Who will still be here in 2030?" frequently surfaced—highlighting the immense challenges facing OEMs today. European brands, in particular, are struggling with the need to catch up in terms of price and technological advancements, while new entrants face the hurdles of building brand recognition, and developing a comprehensive Downstream approach with sales, financing, after-sales, services... capabilities. The Stellantis-Leapmotor partnership, is here particularly interesting as it vastly facilitates Leapmotor's entry into Europe, while allowing Stellantis to pragmatically complete its product line with Electric Vehicles affordable for the mass market. The other Chinese players will need to quickly develop their Downstream, which clearly is an opportunity for European financiers, retailers, workshops, and other service providers. If it has taken decades for Korean OEMs to establish a foothold in Europe, bets are that it will take way less for the Chinese ones...

Tesla robotaxi & Q3 results

Tesla shareholders are used to the ups and downs of the Tesla share following every announcement. At the highly anticipated Robocab event, Tesla unveiled ambitious plans, including a 2-seater, pedal-free vehicle with inductive charging, priced below $30,000 and aimed for production by 2027. The company projected unsupervised self-driving capabilities in California by 2025, pending regulatory approval, and introduced a Robovan concept with seating for 14 but space for up to 20 passengers.

Additionally, Tesla is emphasizing "Optimus," a line of human-like robots intended to streamline digital production costs. Q3/2024 Results: Tesla's vehicle deliveries increased 6% year-over-year to 462,890, though still below Q4 2023's peak of 484,507. Deliveries of the Cybertruck and Model S/X totaled 22,915 units, representing 5% of all deliveries. Automotive revenues rose 2% year-over-year to $20.016 billion, with overall growth driven by a 52% increase in energy storage and 29% in service revenue. Profitability improved with a 16.4% gross margin on automotive production (19.6% including regulatory credits) and an 11% pre-tax margin across Tesla. The energy storage segment achieved the highest profitability with a 31% gross margin. Cost savings were key, as operating expenses dropped and production costs per vehicle reached a record low of $35,100. Regulatory credit revenue also bolstered operating margins, by 4 percentage points.

CVA perspective:

As always, Tesla is a touchstone for where the EV market is going, and where the ICE market is being pulled to. The past quarter showed that Tesla was able to increase margins despite flat / slightly decreasing vehicle prices, which improves its situation, without (yet) solving its growth problem. What is more interesting in this sense is that Tesla now has additional leeway for a new round of price reductions. This seems all the more likely as Tesla has also abandoned plans for a $25k car, opting instead to reduce prices on current models, potentially offering cheaper versions. So chances are that Tesla will double down in its "race to the bottom", increasing yet the challenge for other OEMs to sell enough EVs to meet tighter Fleet Emission targets from 2025. This is coherent with its auto end game, where the human-like Optimus robot progressively replaces factory labor, achieving the most efficient production process imaginable. Tesla and BYD have a clear head start in the race to maximum cost efficiency—placing even greater pressure on traditional OEMs to make radical decisions on upstream and downstream activities. If this bet is quite radical, we find it more realistic than Tesla's bet on Autonomous Driving (catering for the largest part of its market cap). Despite bold announcements, Tesla lags behind competitors like Baidu, which has already deployed 500 fully autonomous robo-taxis in Wuhan, China, and Alphabet’s Waymo, with active robo-taxi fleets in San Francisco and Los Angeles. If autonomous driving has long been overhyped, to then disappear from mainstream strategizing, it will still not move the needle for most players in the near future, but now is the right time to consider as an impacting factor for the medium- / long-term planning of all players in the AutoMobility Ecosystem.

Uncertainties in the field of battery technology

Solid-state batteries, often hailed as the future of EV technology due to their high energy density and rapid charging capabilities, are facing delays and new challenges. Automotive giants, including Toyota and Nissan, have announced advancements, but commercial production remains projected for late this decade, with further hurdles anticipated. Despite solid-state's promising theoretical benefits, substantial technical issues like battery swelling and cell degradation continue to impede progress. Meanwhile, China’s battery innovators, including CATL and Ganfeng Lithium, are developing a middle-ground option: semi-solid-state batteries, combining both solid and liquid electrolytes. These batteries are already used in some Chinese EVs, potentially offering a transitional technology that could meet current market demands more practically. With Chinese firms leading in both semi-solid and traditional lithium-ion technologies, European automakers may need to explore similar approaches to remain competitive / less depedent and adapt to shifting market conditions.

CVA perspective:

Solid-state technology, while revolutionary, faces significant technical and commercial barriers. It won't relieve European OEMs from current or mid-term challenges regarding consumers' confidence in EVs and their TCOs - especially charging and RV related, both topics that are highly linked to the battery. Meanwhile, China is expanding its battery leadership beyond conventional lithium-ion technology, advancing rapidly in both solid-state and semi-solid-state solutions. This not only underscores the competitive advantage of Chinese firms but signals a critical need for European OEMs to intensify their focus on understanding how evolving battery technologies impact the optimal EV architecture and the right development & setting of BEVs in the short- to mid-term. Furthermore, asset owners and risk takers - especially LeaseCos with multi-cycle focus and insurers with high risk loads - must anticipate how pre-dominating but also new battery technologies will affect lifecycle management and residual values. All players need a clear strategic understanding that enables them to act quickly and react flexibly to changing developments in order to be competitive in their home market and to successfully expand their EV business.

Qorus-CVA RV & next event

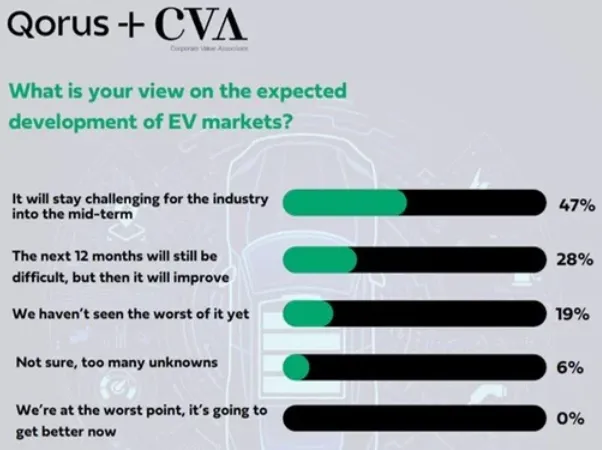

The Qorus-CVA Mobility Community held a well-attended Webinar on the hot topic of EV Residual Value (RV) developments across Europe. Data and insights from Christoph Engelskirchen, Chief Economist at Autovista, Ian Plummer, Commercial Director at Autotrader and Sam Heymans, the founder of the Used Car Leasing player Lizy showed that the management (and especially mitigation) of EV RVs will remain a critical topic for the sector for at least the short-term, where numbers of de-fleets are only just starting to grow.

This was also felt by our participants, 75% of whom believe that EV markets will still be challenging for at least the next 12 months. Hence CVA believes that the topic of multi-cycle is strategically important for all players impacted by RV risk. Taking an end-to-end asset management role "in-house" is the only way to be able to truly manage a long-term RV curve without market price swings. Lizy provided us with a case example of a player who is doing just that with profitable used car 2nd and 3rd lease cycles in several European countries.

Next event:

Our next webinar will be on November 12th at 10am CET, on the topic: Bridging traditional and emerging mobility: the strategic role of banks and insurers. We have the please to introduce Delphine Garcin-Meunier, Head of Mobility and International Retail Banking & Financial Services at Société Générale, who will be the Chairperson of the Mobility Community going forwards. You are all very welcome to join us! Register Now!

Authors

Mobility community

With Qorus memberships, you gain access to exclusive innovation best practices and tailored matchmaking opportunities with executives who share your challenges.