Digitalization in financial services in South Africa: Is it worth the squeeze?

In South Africa, financial institutions are undertaking some incredible digitally-focused work. They are innovating with customers at the core of their efforts.

In partnership with

Oliver Wyman

Oliver Wyman is a leading global management consulting firm that combines deep industry knowledge with specialized expertise in strategy, operations, risk management, and organization transformation.

Digitalization is transforming banking as we know it. At Efma, we make a concerted effort to document and highlight the most impressive initiatives from the financial services industry. In this way, we can help our membership — and beyond — adapt to rapidly changing customer preferences and stay ahead of the curve.

In South Africa, financial institutions are undertaking some incredible digitally-focused work. They are innovating with customers at the core of their efforts. They are utilizing data and AI to deliver personalized experiences and on-demand banking. With increased competition from neobanks and big tech, it is imperative for institutions to continue reimagining financial services. As you will see in the following pages, there is some truly impressive work going on in the African nation.

We were happy to partner with Oliver Wyman to produce this report. We want to thank them, along with all contributing institutions, for providing their expertise and insight on the current and future state of digital banking in South Africa. I am sure you will find this report informative and illuminating.

Introduction

Digital has been rising up the executive agenda in South Africa’s financial services industry for the past decade. It has been the major driving force behind tremendous changes across the industry, allowing innovation and healthy competition to flourish.

While South Africa’s traditional financial services groups are focused on digital transformation, new digital-first competition in the form of Discovery Bank, TymeBank and BankZero has entered the fray.

Digital adoption has picked up across the board, with notable innovative moves from both incumbents and new entrants. Prompted by emerging technology, greater competition, and increased customer expectations, customers can now enjoy benefits such as opening a bank account in minutes, executing simple transactions using WhatsApp, or conveniently completing cash handling services through their local grocery stores. Digitalization has also improved financial inclusion by lowering barriers to access through the emergence of low/ zero cost banking, with new neo-banks operating on lean cost models supported by superior next generation technology.

Digitalization provides an opportunity for financial services organizations to improve operational efficiencies. Streamlined services on digital platforms have significantly reduced the turnaround time for menial tasks, and in turn improved the customer experience — whether at a branch, on the app, or online.

Beyond traditional financial services, South Africa has seen new non-financial services players tap into the market, such as MTN’s mobile money operations, MoMo, which aims to build on the success that mobile money has had in the rest of Africa, particularly in East Africa with the likes of M-Pesa.

The South African Reserve Bank (SARB) has also kept abreast of digital developments in the financial services industry. In response and anticipation of the rapid growth in fintech, the SARB set up a fintech unit in 2017 to explore its impact and implications. It is actively promoting innovation and allowing new players to enter the financial services industry, creating innovation-friendly structures and sandboxes to drive innovation in areas across the digital spectrum.

What is digital

For the purpose of this report, digital and digitalization are defined as the integration of technology and data into all areas of an organization to improve business operations and customer outcomes through process automation, data analytics, interfaces, seamless integrations and connectedness, artificial intelligence and machine learning.

Covid impact

Along with changing consumer behaviors, COVID-19 has caused the most recent acceleration in digital adoption. The pandemic forced everyone into a new normal — it changed how we communicate and engage with each other, how we consume, how we keep ourselves busy, how we support one another, and how we rely on technology to enable all of this.

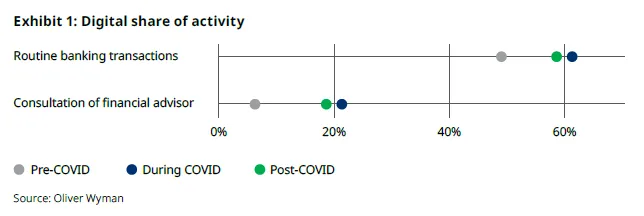

In the financial services sector globally, COVID-19 has been a catalyst in changing digital behavior, with lockdowns and temporary bank closures forcing a shift away from traditionally branch-led activities. South Africa is no different.

Many banks have argued that customer behavior does not change overnight and aligned their change roadmaps to this assumption. But the current crisis has taught us beyond any doubt that behaviors can change in a heartbeat. One of South Africa’s largest insurers noted that from the start of 2018 to the end of 2020, the number of customers transacting on its mobile application grew by 470%. Separately, one of South Africa's largest banks experienced a growth of more than 200% in digital transactions between January and August 2020, compared with the previous year.

The increase in digital usage is set to remain, as highlighted in the Oliver Wyman report Ready or Not: The Staying Power of Our Digital Habits

The future

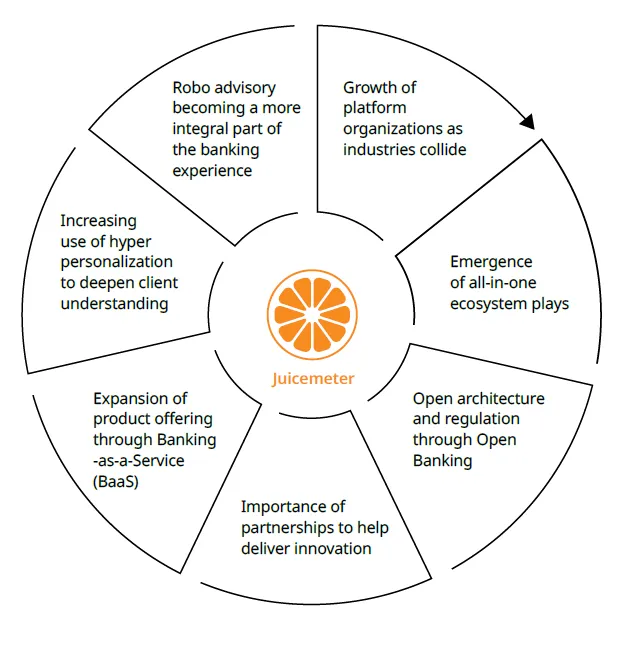

While the benefits of going digital are already significant, there remains untapped value within the South African financial services industry. We have identified seven plays where digital can deliver significant incremental value and transformational impact — and assessed each play using a customer and shareholder “Juicemeter” rating scale to consider potential value left to be unlocked for either stakeholder. In some cases, these plays are beginning to be explored across the South African market, but in others the opportunities have not been explored at all. This list is not exhaustive, but lists areas with significant potential for value creation.

What is a platform organization?

A platform organization is a business based on enabling value-creation through interactions between external producers and consumers. The platform provides an open participative infrastructure for these interactions and sets governance conditions for them. (Source: TheMarketingJournal.org, “The Platform Revolution” Interview)

The distinction between traditional financial services and other industries is narrowing globally. In order to capitalize on this — and navigate the threat of non-financial services players moving into spaces traditionally dominated by banks — financial services players can move to create digital platforms offering products and services beyond their original value chains.

Digital plays a critical role in making this possible. It enables multiple connections with other industries to be formed rapidly to quickly adapt to changing market and customer needs. This move requires a complete change in philosophy of what a financial service provider offers and an overhaul in terms of ambition.

Doing this successfully involves creating a platform that allows partner businesses to plug in and out of easily. Successful platforms create the opportunity to gather valuable data across various areas to create insights and datasets that can be monetized.

Another key success factor is speed. If the digital strategy is not executed quickly, the level of competition rises and first mover advantages diminish. According to an executive of one of Africa’s largest insurance groups, “this game is won on speed.” For example, how the network effects of Facebook led to its ultimate success as people sought to join a platform that all their friends were on is well known. The same applies for banking and insurance platform winners — those that move first and can competitively solve consumers’ financial and non-financial needs on one platform will be able to attract and retain consumers.

Becoming a platform organization presents a win-win, both for the organization that owns it and the customers who plug into it. By allowing non-financial service organizations into the financial services ecosystem, financial services players can position themselves as being more than just banking and insurance partners to their customers, instead serving a client’s end-to-end needs from within a single platform. This provides convenience for the customer and additional revenue streams for the platform owner.

Customer expectations are changing and they are beginning to want all their needs serviced on-demand and in one place. This provides organizations with the opportunity to orchestrate ecosystem plays in broad areas of their customers’ lives (for example, buying a home, or healthcare), and to build an offering that services their needs end-to-end. This is considered a digital ecosystem and brings increasing customer value onto the financial service providers’ platform.

Successful ecosystem plays hinge on intuitive user interface design (UI) and user experience (UX). Beyond this, digital allows “on-demand” expectations of customers to be delivered through effective interfacing of relevant products and services, improving customer experience in the process.

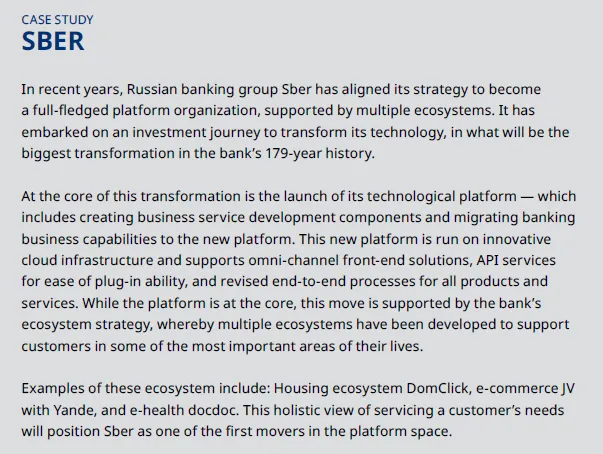

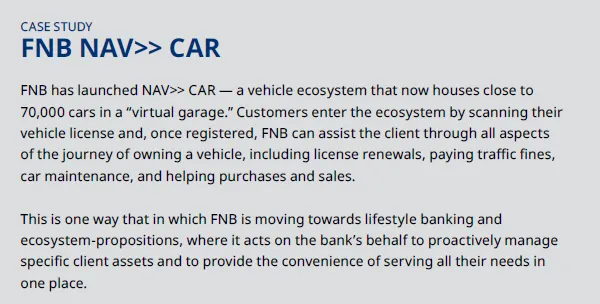

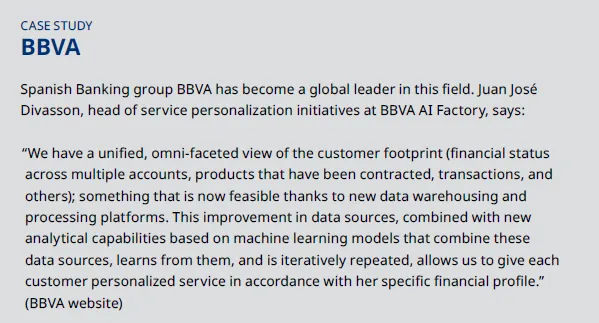

For the ecosystem orchestrator, value is derived from additional revenue streams; and the ecosystem appeals to potential customers as it offers a holistic service. Such plays have been made globally by both technology companies (e.g. Google, Uber) as well as financial services players, with the extension of their products and services through adjacent partners to deliver end-to-end services to customers. One best-practice example is PingAn, a large insurance player in China, which created multiple ecosystems around auto, housing, and health. Another example is Spanish banking group BBVA, who developed an ecosystem around its mortgage business to provide offerings positioned around home purchases.

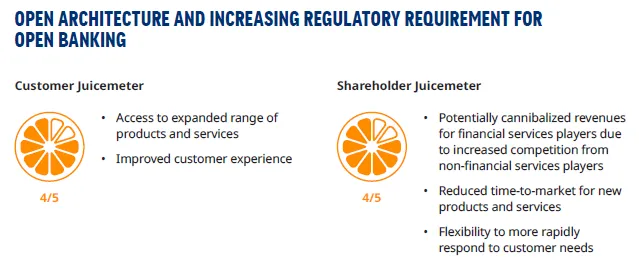

Globally, digital open architecture is the new frontier in the push to transform the financial services industry. Open architecture is a term used to describe the use of an Open Application Programming Interface (API), a software intermediary that allows application programs to interact with each other and share data.

The move to a platform organization and ecosystem play is only successful if it provides value through efficiency of service delivery to the customer or a greater flexibility to respond rapidly to changing consumer expectations. This rapid response can be delivered through plug-in capabilities provided by open architecture, which will create an opportunity for organizations to harness this capability by transforming their IT architecture to accommodate open APIs. Whilst internal APIs have played a role in the financial services industry for a number of years, there is a growing requirement to support both public and partner APIs that will allow external partners and developers to build innovative products that can easily and securely connect into bank’s and insurer’s previously walled data environments.

The move to open architecture has led to increasing regulatory pressure on the concept of open banking. Open banking drives banks to change their business models and provide access to their data using APIs, strictly controlled by the regulator. This allows banks, technology companies, fintechs and others open access to each other’s data to begin building products and services. This has been rolled out in some countries and regulator support is boosting the move — such as the revised Payment Services Directive (PSD2) in Europe and the Open Banking initiative in the UK, Russia, Brazil, Australia and other markets.

Open banking empowers customers by allowing access to, use of, and benefit from their financial data. It has its risks concerning data ownership and privacy. As such, open banking has become an important topic on regulators’ agendas recently. The move to complete open architecture will require active regulator support through the provision of guidelines for licensing access to data and ensuring consumer protection.

While the South African regulator has reportedly1 started industry consultations with a view to safeguard consumer data and manage cybersecurity risks specific to open banking, there is yet to be any official move regarding the open banking regulation. As open architecture becomes an enabler of digital growth in the financial services industry in South Africa, it is a subject that will likely remain top of the agenda and be addressed by the regulator in the very near future.

Financial institutions are increasingly realizing that not all digital capability needs to be built and owned in-house. One approach to building a feature-rich proposition and increasing the reach of an organization is to adopt a partnership strategy. The partnership strategy should be viewed as an accelerator to offering meaningful and value adding capacity to the financial services products and capabilities.

The notion of a partner simply being a vendor or supplier has been replaced by partnership models, where co-creation and value sharing are experienced by both parties. This relationship needs to be actively managed by both sides and should resemble a partnership business model.

Success in building a partner-friendly organization is underpinned by having the ability to seamlessly onboard and connect with third-parties through an effective API marketplace. In the future, procurement capabilities within organizations will need to develop — helping facilitate onboarding of partners, allowing active partner management, and ensuring continuous communication and learning between parties. Additionally, a future partnership strategy will need to allow organizations to measure the impact and value that partners are having (for example, increase in cross sale rates, higher application downloads, and others). This will allow for timely decision-making where results or value delivered by partners may be lagging.

By choosing partners strategically, financial institutions can break down silos and navigate untapped ecosystems, which in turn can unleash pockets of innovation for the benefit of customers. For financial institutions, this brings the opportunity of further revenue streams through diversified offerings.

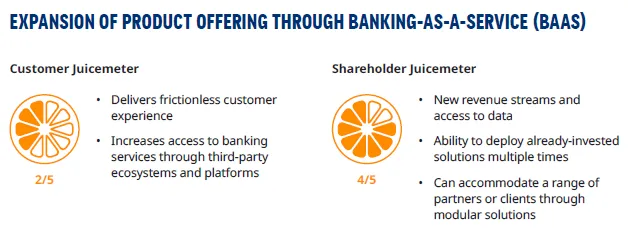

Banking-as-a-Service (BaaS) allows banking institutions to commercialize their capabilities and scale them into external, third-party ecosystems. Examples of BaaS include modular banking processes such as payments or credit being delivered to third-parties through API-driven platforms. For the end user, this could mean being able to obtain credit when paying for shopping online or purchasing a holiday, for example.

Including BaaS in the digital strategy provides the opportunity for access to low cost incremental value based off digital assets that have already been developed or invested in internally. Given that BaaS can operate off a model of “build once, deploy multiple times,” it also allows scalability.

Benefits to the third-party player are twofold. First, it enables them to offer financial products and capabilities on their own platforms, which adds incremental revenue to their sales and deepens customer relationships through a one-stop-shop solution. Second, it allows the delivery of these products to market at increased speed with limited overheads and oversight.

Banks and insurers derive value in the form of new revenue streams or additional access to customers and data in new ecosystems and customer segments. This strategic move can also provide financial services players an early advantage if they form partnerships with non-financial services organizations looking to enter the space.

A key benefit of digitalization is the ability to harness the data collected to provide a more personalized customer experience. By utilizing data beyond traditional transactional data, insights can be mined to give a broader view of the client and their journey. This can be done using machine learning or advanced algorithms to accurately profile customers.

These advanced analytical techniques have started to put the concept of “a segment of one” into action. A segment of one is the idea that each customer is unique, and that given the capabilities of modern technologies, one doesn’t have to apply a blanket approach to solving customers’ problems. For example, instead of sending a savings campaign to all millennials (a segment of millions of consumers) one could dynamically tailor content to each individual based on their income, interests, or online activity (segment of one).

By accurately identifying customer pain points or opportunities, digital solutions can be developed to position products in real-time. This can be done on a day-to-day transactional basis or periodically through major life events, such as buying a home or getting married.

Opportunities include:

• Positioning more relevant solutions to customers, and targeting their current needs or

financial goals. This will improve client satisfaction and increase product penetration

• Using insights from data to nudge customers through push-notifications, to make choices that align to their short- or long-term goals (for example, increasing health insurance for a new child or saving for a home)

• Dynamic interest rates and savings incentives for meeting longer-term goals. An example of this is Discovery Bank, which has introduced behavioral banking, that incentivizes customers to meet their savings and spending goals by offering dynamic interest rates

More banks are now also providing financial advisory services as the need for financial advice among South Africans is growing. As awareness of money management and financial wellness improves, customer expectations shift and they become more engaged with financial decisions. This shift will be further exacerbated in the future as the middle-income segment in South Africa grows.

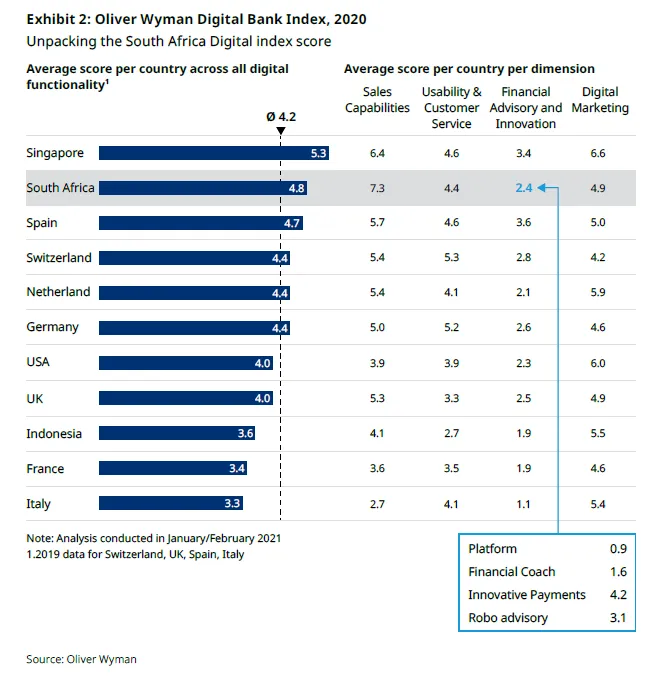

There is a notable deficiency in robo-advisory services provided by South African banks, as illustrated in the 2020 Oliver Wyman Digital Banking Index Study. The study looks at 115 financial institutions from 11 countries to create an index along the breadth and depth of the digital (online and mobile app) offering from customers’ perspective. One specific area where South Africa is significantly behind is “financial advisory and innovation,” which includes the two categories “financial coach” and “robo-advisory.” Robo-advisory is the process of automating financial advice based on customer data, and, of the nine South African banks included in the index, a majority (five) were lagging in terms of their robo-advisory offerings.

Digital can help improve banking and insurance propositions in this space through the execution of robo-advice. This service can enable the provision of premium financial advice to all segments, advice that has previously only been available to the affluent segment or those with access to private banking. Using data analytics and algorithms, robo-advisory can assist customers reach their financial targets without the need for time-consuming human interaction and processing.

The growing demand among South Africans, the low headcount required, and the accuracy of data processing, make the move to robo-advisory an excellent value-creating opportunity for financial services institutions.

Closing remarks

Digitalization has resulted in the creation of great value in the financial services industry in South Africa. However, there is still a lot more juice to be squeezed. While the seven opportunities outlined in this report help sketch the path that financial services players can take to generate more value out of digital, the future is constantly changing.

Being digital is not a destination, it’s an ongoing journey.

While the future looks bright with value-adding opportunities for both the customer and the financial services industry as a whole, these opportunities do not come without risks and threats. The most notable are cyber and data security threats, risks that financial institutions must understand and protect themselves against. The potential reputational and financial damage that can result from a cybersecurity incident or data breach can be enough to sink an institution.

Beyond cyber risks, the South African financial services industry will have to manage massive internal transformational change to overcome the hurdles of legacy technology and outdated business models.

Additional risks such as compliance, connectivity, and access to digital devices in South Africa are among a longer list of challenges that will need to be managed in order to smoothly navigate the new world of opportunity that digital continues to open up to financial services players.

Digital winners globally did not have all the answers right off the block. They failed fast and kept an open mindset to continue learning. Keeping up with customer expectations and needs will always be the aim, but how competitive one is will come down to how bold they are with their digital strategy and how focused they are on transformation.

Interviews

South Africa is home to a financial services landscape where digital — and all that is encompassed in that word — is driving major change. When thinking of digital front runners, fintechs and big techs often come to mind, but in South Africa some of the biggest changes are being driven by banks. Increased customer engagement, impressive new offerings, and reimagined business models are just some of the ways digital is upending financial services in the country.

In order to get an inside look on what’s really taking place, we spoke with top executives who are leading digital transformation efforts at their respective institutions. As you will see in the following interviews, banking and insurance executives are keenly aware of both the opportunities and challenges that come with digital banking. Competition may have increased, but so has the recognition and understanding of South African institutions of the need to innovate for their customers.

We asked these executives what is driving their digital agenda, what types of value they are seeing from their investments, and what more digital has to contribute. Answers to those questions and further insight are in this report. Digital banking is disrupting and transforming the world of financial services. Find out how South African financial institutions are setting the standard.

Interviews

Download your study now

Leverage community expertise to redefine finance

Our communities cover diverse topics such as digital transformation, SME finance, or Embedded insurance, providing a platform to learn from industry experts and peers.