AutoMobility Insights - December 2024 edition

The latest news from the automotive industry curated and commented by the experts at Corporate Value Associates (CVA).

In partnership with

Corporate Value Associates

Corporate Value Associates is a Global Strategy Boutique supporting market leaders in creating value through its customer-centric approach.

This year ends with a host of “earthquakes”, which show that progressive evolution is not enough to manage the ongoing tectonic shifts. There is Carlos Tavares exiting his position, rumors of a mega merger between Honda, Nissan, potentially Mitsubishi (and Renault…?), news of structural adaptation of VWAG…

The topics chosen below are of no lesser interest. We cover the (for the time being) last chapter of OEMs engaging in the agent model, with Europe's largest players, VWAG and Stellantis practically ending their short term development. Focusing on customer acquisition, a new agreement with Hyundai opens a further attempt by Amazon to take a role in new car sales, in a market where purchasing processes increasingly start online. But will Amazon’s new concept succeed getting from traffic to sale? Another topic between auto & tech concerns the exit of GM from Autonomous Driving, which has become a “risky bet” perhaps too heavy to carry by OEMs who have "more short-term" battles to win. Finally, the last Qorus-CVA Mobility Community webinar of the year has focused on New Entrants (e.g. Chinese OEMs) in Europe, with options for Financial Service players to position as partners. Feel free to listen into the recording you can access via the Qorus site.

We hope that the snippets of fundamental change have been useful for accompanying you during this full and demanding year. Our entire AutoMobility Team wishes us all a quiet holiday season, and a good start into 2025, a year which is sure to come with additional challenges!

As we plan for 2025, we want to hear from you! What topics matter most to you? Share your feedback using this survey link, which includes some predefined topics and a free text option. Your input will help us ensure our newsletter delivers the most relevant insights and thought-provoking content to support your decision-making and success in the year ahead.

VW Germany discontinues the BEV agency model

Volkswagen (VW) has announced it will discontinue its agency sales model for electric vehicles (EVs) in Germany, citing its lack of economic viability compared to traditional dealership sales. The agent contracts will be cancelled still in 2024 and EV sales will be re-integrated in the existing dealer contract as of 2026. This decision reflects VW's commitment to its dealer network and rejection of direct sales without dealer involvement. VW will however not entirely retreat from its plans for an agency model and will continue to test full agency model in Sweden and Ireland.

VW dealers had previously criticized the agency model due to reduced compensation and unmet promises regarding a shift of costs to the OEM, which led to frustration. Other VW Group brands like Skoda and VW Commercial Vehicles have also paused their transitions to the agency model, while Audi has adopted it in some European markets but has no plans to implement it in Germany.

CVA perspective:

The Agent model has initially been started by OEMs to avoid cannibalization between dealers, to get access to customer data and… to improve OEM margins. After initial hype amplified by a clement Covid-period, most OEMs have pulled back, with essentially only Mercedes-Benz and BMW / Mini pursuing actively. The reason for the U-turn: Just modifying the contract and the margin split does of course not generate a viable model, which requires sufficient commercial “push” where “pull” is not enough, management of a host of operational activities at the dealership... Also, roles & responsibilities and margins have not been fully re-balanced, not giving a viable perspective for Dealers. But most importantly, efficiency and performance improvements only possible with an integrated model have not been addressed. OEM communications suggest that the agent model is not completely abandoned (e.g. VWAG continuing prototypes in Sweden and Ireland), but will not be used to take us through the coming challenging years. A fully integrated and seamless Downstream will likely remain the long-term perspective in order to increase customer impact and operational efficiency. The challenge is to develop a model that works out for all stakeholders (OEMs, NSCs, Dealers) and … the end customer. This will remain the main guideline for Downstream development in the coming years.

Amazon US starts to sell new cars

Amazon has (re-)entered the car sales market, initially partnering with Hyundai to offer new vehicles on its platform in 48 U.S. cities, including San Francisco and Washington. Customers can configure, finance, and purchase Hyundai models directly on Amazon, with options to trade in old cars using an online valuation tool. While Hyundai is the first partner, Amazon plans to expand its offerings to include other manufacturers and dealers, aiming to make car buying more transparent and customer-friendly.

Though purchases are made online, vehicles must be picked up at local dealerships, which remain part of the process. While financial details of dealer participation are undisclosed, early buyers will receive a $2,300 Amazon gift card.

The move highlights the shift towards digital car sales, a trend led by brands like Tesla and Rivian, which bypass dealers entirely. However, most manufacturers, including Amazon’s new partner Hyundai, still rely on a hybrid sales model that integrates dealerships, reflecting consumer preferences for a combination of online and in-person services. For Hyundai the partnership marks another significant collaboration, following its recent deal with Waymo to supply Ioniq 5 models for its robotaxi service.

CVA perspective:

Pure online New Car sales have long been forecast to pick-up massively, but reality has remained behind expectations. Nevertheless, progress on online / mobile channels has allowed customers to benefit from more or less integrated multi-channel approaches, more designed to improve an essentially offline process than full online capability. The increasing role of online for starting the customer journey and comparing offers makes leveraging "Traffic Giants" like Amazon an obvious choice. It is however not certain that adding “the best of both worlds” automatically results in something that functions well. There are a number of additional critical ingredients such as product (simplicity…), engagement (flexibility…), Customer Journey (adaptation to clients…) online-offline handover…. A key issue is also pricing, where standard prices avoid haggling and cannibalization, but also limit volume and margin capture. In-depth understanding of customer and offer options is key. It will be interesting to see how this new edition of the Amazon model will fare...

GM ends its autonomous taxi dreams

General Motors (GM) has announced the end of its Cruise robotaxi program, surprising many industry observers. Cruise Automation, the self-driving car startup acquired by GM in 2016, will be absorbed into GM's operations and refocused on developing advanced driver assistance features for personal vehicles. The move was announced via a Slack message from Cruise CEO Marc Whitten. Cruise had faced challenges and regulatory set-backs including the loss of operating permits in California after a high-profile accident. This has let to a delay, layoffs and changes in leadership. Earlier this year, GM had already signaled a shift by shelving its custom-built Origin robotaxi and opting for a next-generation Chevrolet Bolt to simplify scaling efforts.

While Cruise had recently resumed testing in cities like Phoenix and Dallas and had planned to launch with Uber in 2025, GM’s decision reflects its pivot away from robotaxis to focus on more feasible assisted driving vehicle applications. GM initially projected tens of thousands of robotaxis generating $50 billion annually by 2030.

CVA perspective:

After significant hype about Robotaxis in the last decade, spirits have become more divided. Between abandon (Ford / VWAG with Argo AI, GM with Cruise Automation…) and Robotaxi potential making up a large part of an OEMs stock value (Tesla). For OEMs, abandoning “moonshots” seems to be a safe bet these days, especially as they are confronted with difficult situations at least in some geographies. They also see the need for continuing investments to remain in the game with the Waymo, Zoox, Tesla and a long list of less known players. And of course Chinese players, such as Baidu, supported by a an easier regulatory environment. On the other hand, the innovation challenge is currently shifting from Electromobility to Vehicle Intelligence, which makes of Autonomous Driving potentially a major differentiator, at one point. So even for OEMs the decision to exit the AD race may not be that obvious.

A key to understanding these moves are probably different shareholder expectations. GMs share-price was barely affected by the news, with investors likely preferring the USD 1bn p.a. being spent on building competitive Smart BEVs rather than into an AD bet. So it seems that there is a real question of who is the best owner of AI ventures, which may better fit with Tech players than with EBITDA oriented OEMs, Tesla being here a clear outlier.

Qorus mobility event

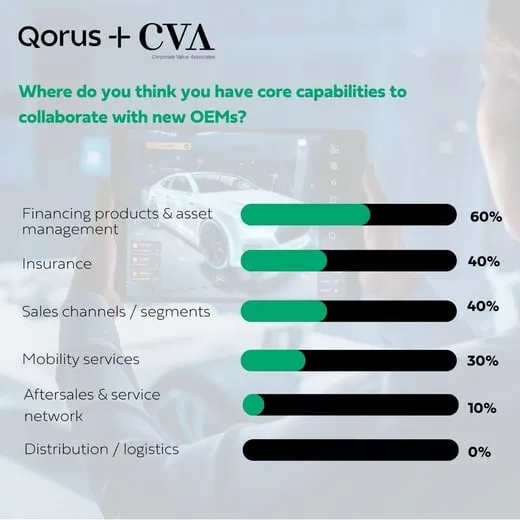

We wrapped up our 2024 webinar series with a discussion on: "Emerging OEMs from Asia and America: Opportunities and challenges for financial institutions". Whilst a lot of the recent weeks have been all about doom-and-gloom in the auto industry, Chinese OEMs in particular continue to have a strong software-led EV product for the European market. Very strong on the asset, where they need more support is on the more mature European downstream model vs China, including distribution channels / segments, financing, aftersales, insurance and other services. Our speakers from Société Générale, Crédit Agricole and Allianz Partners all have strategic partnerships with these new entrants and shared some insights on how they differ from established OEMs (not significantly in terms of long-term mix of omni-channel, multi-customer needs!). One thing we highlighted was that although the audience may see the basic core capabilities as a priority to work with new entrants, positioning as a strategic partner will likely need a more holistic support e.g. how to solve some of the aftersales & services challenges during scale-up.

Next event:

We'll be back on January 28th at 10am CET with a webinar on: "Electromobility: Batteries as the key Asset for making it work". Should be an interesting discussion, as part of the asset mgmt. equation that is most critical to EVs but not that well-understood / managed today at-scale. Do already register to join us / receive the recording & materials. In the meantime, we wish you a restful end to the year!

Authors

Mobility community

With Qorus memberships, you gain access to exclusive innovation best practices and tailored matchmaking opportunities with executives who share your challenges.